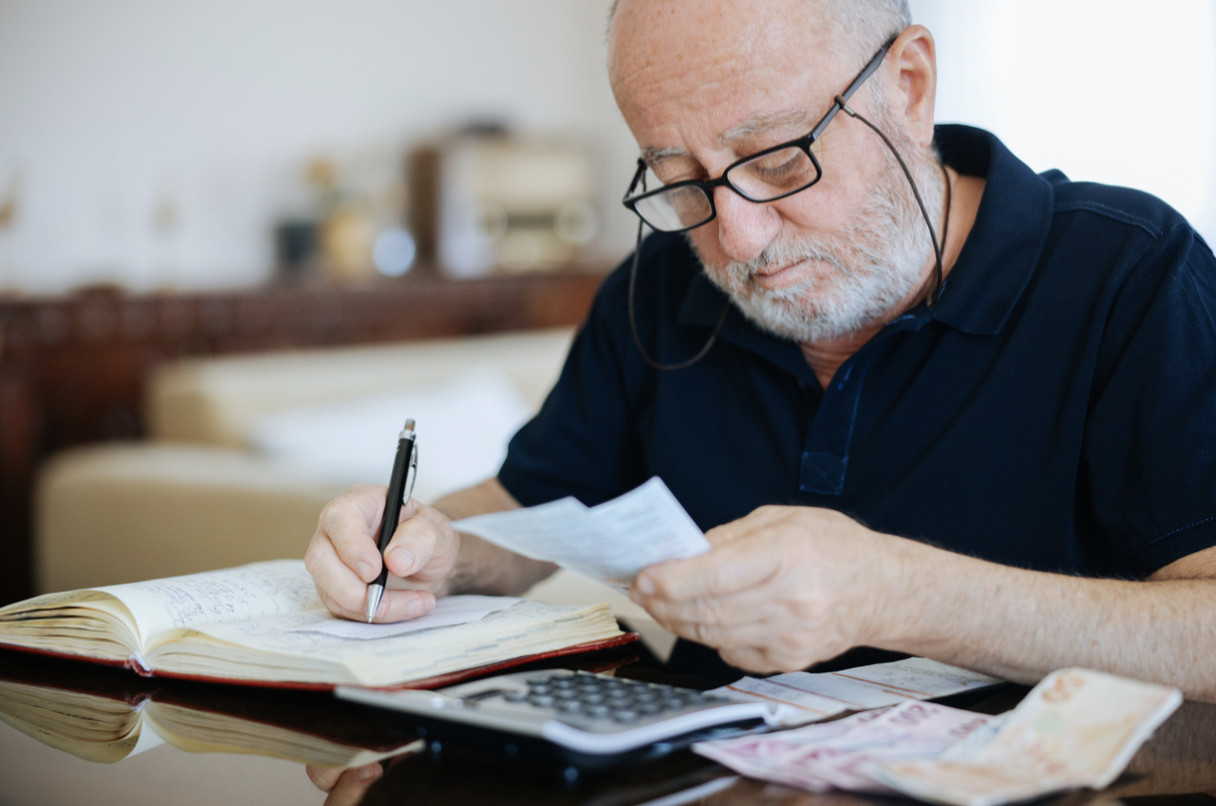

Building a Retirement Budget You Can Rely On

A retirement budget helps you balance your savings with future living costs so you can maintain financial stability without fear of running out of money. By estimating income sources, accounting for healthcare, and planning for lifestyle choices, you create a roadmap that keeps your retirement years secure and enjoyable. This article works as a retirement budgeting guide to help you take the right steps toward financial peace of mind.

Table of Contents

The Role of Budgeting in a Successful Retirement

How to Create a Retirement Budget Step by Step2.1. Identify Reliable Sources of Retirement Income2.2. Estimate Your Living Expenses in Retirement2.3. Account for Healthcare and Unexpected Costs2.4. Adjust for Inflation and Lifestyle Choices2.5 Test and Refine Your Retirement Budget

Practical Tips to Keep Your Retirement Budget on Track

Final Thoughts and Key Takeaways

The Role of Budgeting in a Successful Retirement

Many people underestimate the financial shifts that come with retirement. The steady paycheck stops, but expenses continue. What changes is how those expenses are funded. A retirement budget outlines how your savings and income will support the lifestyle you want throughout your retirement years.

Failing to map out this plan can lead to overspending in the early years, leaving too little for later stages of life when healthcare costs or options like assisted living in Calgary may be needed. Retirement budget planning ensures your finances provide clarity, reduce stress, and support decisions that align with your goals.

How to Create a Retirement Budget Step by Step

Identify Reliable Sources of Retirement Income

The first step is to know what money you can count on. Retirement income often comes from a mix of sources:

Government programs such as CPP, OAS, or Social Security.

Employer pensions if available.

Personal savings and investments like RRSPs, 401(k)s, or brokerage accounts.

Rental income or part-time work if you plan to stay active.

By writing down each source and estimating monthly income, you establish a clear picture of your financial foundation

2. Estimate Your Living Expenses in Retirement

What you spend now may not reflect what you’ll spend in retirement. Certain expenses may go down, such as commuting, work clothing, or mortgage payments, once the house is paid off. Others may rise, like leisure travel, hobbies, or healthcare.

Common expense categories to consider:

Housing (rent, property taxes, maintenance, utilities) Housing is often the largest expense in retirement. Some retirees stay in their current home, while others consider retirement communities with support services and predictable costs. Options likeThe Manor Village at Garrison Woods provide amenities and structured living that can simplify budgeting and reduce unexpected expenses.

Food and groceries Food costs may change in retirement depending on how often you eat at home versus dining out. Planning a realistic grocery budget and factoring in occasional meals out helps avoid surprises and ensures nutrition needs are met without overspending.

Transportation (car costs, insurance, public transit) Transportation costs often decline if commuting decreases, but car maintenance, insurance, and occasional travel should still be included. For retirees who enjoy road trips or frequent outings, these costs can remain significant and need planning.

Healthcare and insurance premiums Healthcare becomes a larger portion of expenses as you age. Routine medical care, medications, dental visits, and insurance premiums should all be accounted for. Including a dedicated healthcare fund or considering long-term care coverage can protect your savings.

Leisure and travel Many retirees spend more on travel, hobbies, or social activities. Being realistic about the lifestyle you want and its costs ensures your budget reflects your priorities without stretching your resources.

Debt repaymentsAny remaining debt, such as credit cards or loans, should be included in your retirement budget. Paying off debts before retiring, when possible, can reduce monthly obligations and increase financial freedom.

To make this easier, some people use a retirement expenses calculator to estimate how much they’ll need each month. Creating a detailed list helps avoid underestimating future costs.

3. Account for Healthcare and Unexpected Costs

Why should healthcare be prioritized in your budget? Because it often becomes the largest expense later in life. Medications, treatments, dental care, and long-term care facilities can quickly erode savings.

To prepare, consider:

Setting aside a dedicated healthcare fund.

Looking into long-term care insurance.

Including a cushion for emergencies, such as home repairs or family support.

This extra layer of budgeting for retirement prevents sudden financial strain.

4. Adjust for Inflation and Lifestyle Choices

Prices do not stay the same over 20 or 30 years of retirement. Inflation steadily reduces purchasing power, meaning you’ll need more money in later years to buy the same goods and services.

Similarly, lifestyle choices matter. For example, regular travel abroad may double or triple your leisure budget compared to staying local. Being realistic about your goals and their costs helps your budget reflect the retirement lifestyle you want.

5. Test and Refine Your Retirement Budget

How can you know if your retirement budget will actually work? One effective method is to test it before retiring.

Trial Run: Try living for six months on your projected retirement income.

Gap Analysis: Track where you overspend or under-budget.

Revisions: Adjust savings goals or spending expectations accordingly.

Testing provides real-world feedback, helping you enter retirement with confidence.

Practical Tips to Keep Your Retirement Budget on Track

Even the best retirement budget requires ongoing attention. Here are strategies to keep it working:

Automate withdrawals from retirement accounts to mimic a paycheck system.

Reassess every 2–3 years to adjust for changes in market conditions, health, or lifestyle.

Diversify income streams to reduce risk from any single source.

Avoid overspending early so funds last for the long haul.

Seek professional advice to model different scenarios, such as varying retirement ages or healthcare costs.

Small adjustments made early can prevent financial stress later.

Key Lessons for Building a Stronger Retirement Budget

A retirement budget gives you control over your finances and ensures your money lasts throughout your retirement years. Listing your income sources, planning for housing, healthcare, and daily costs, and factoring in inflation creates a clear financial path for your retirement years.

The most successful retirees are those who review their budget regularly, adapt as circumstances change, and prioritize long-term stability over short-term spending. Start planning today, and give yourself the peace of mind that comes from knowing your finances are ready for the years ahead.